Knowing how to read financial statements is essential because it allows investors to assess a company’s true profitability, financial stability, and growth potential before making investment decisions. Understanding these documents helps investors avoid risky companies, spot hidden strengths or weaknesses, and make smarter choices to maximize returns.

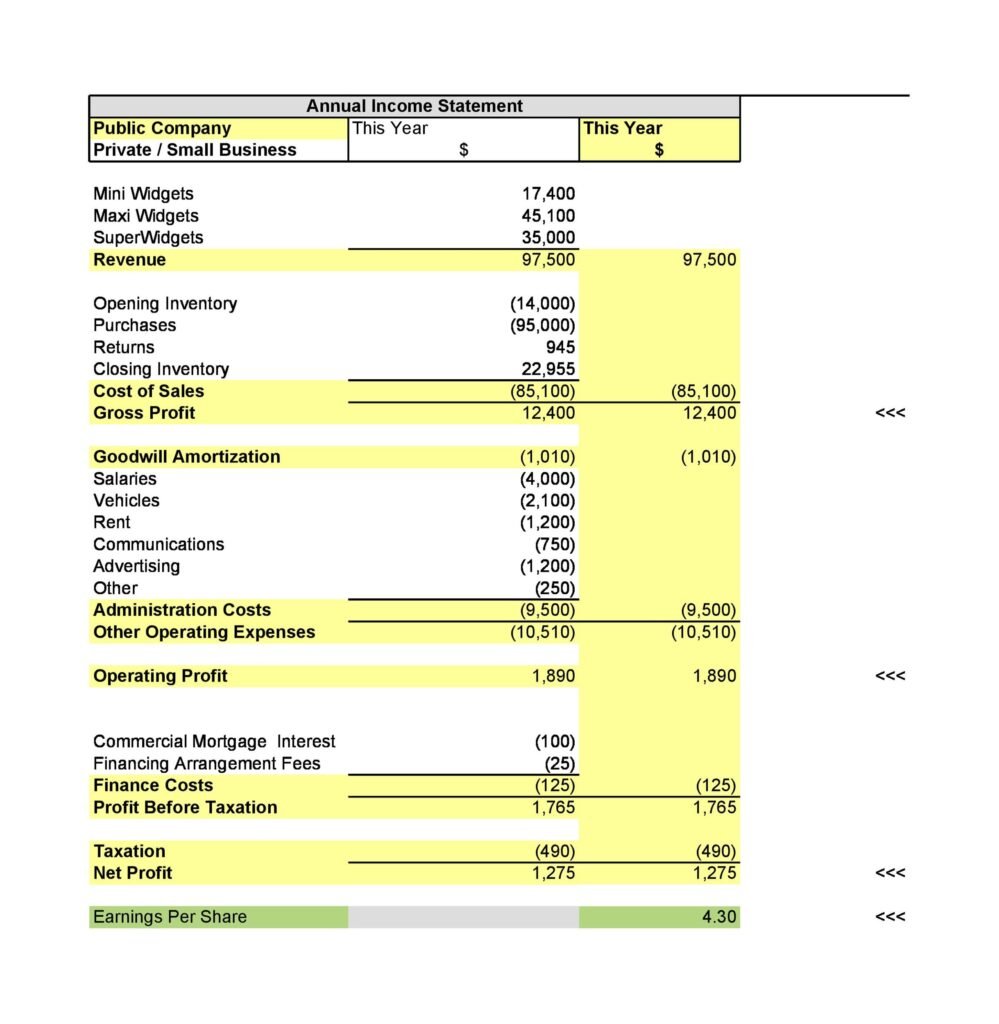

INCOME STATMENT

Purpose: summarizes a company’s revenues, expenses, and profits or losses over a specific period (such as a quarter or year). It tells you how much money the company made and spent, and ultimately, whether it was profitable.

Purpose: This statement details the changes in equity for the reporting period. It explains how the company’s retained earnings, share capital, and other equity items change over time.

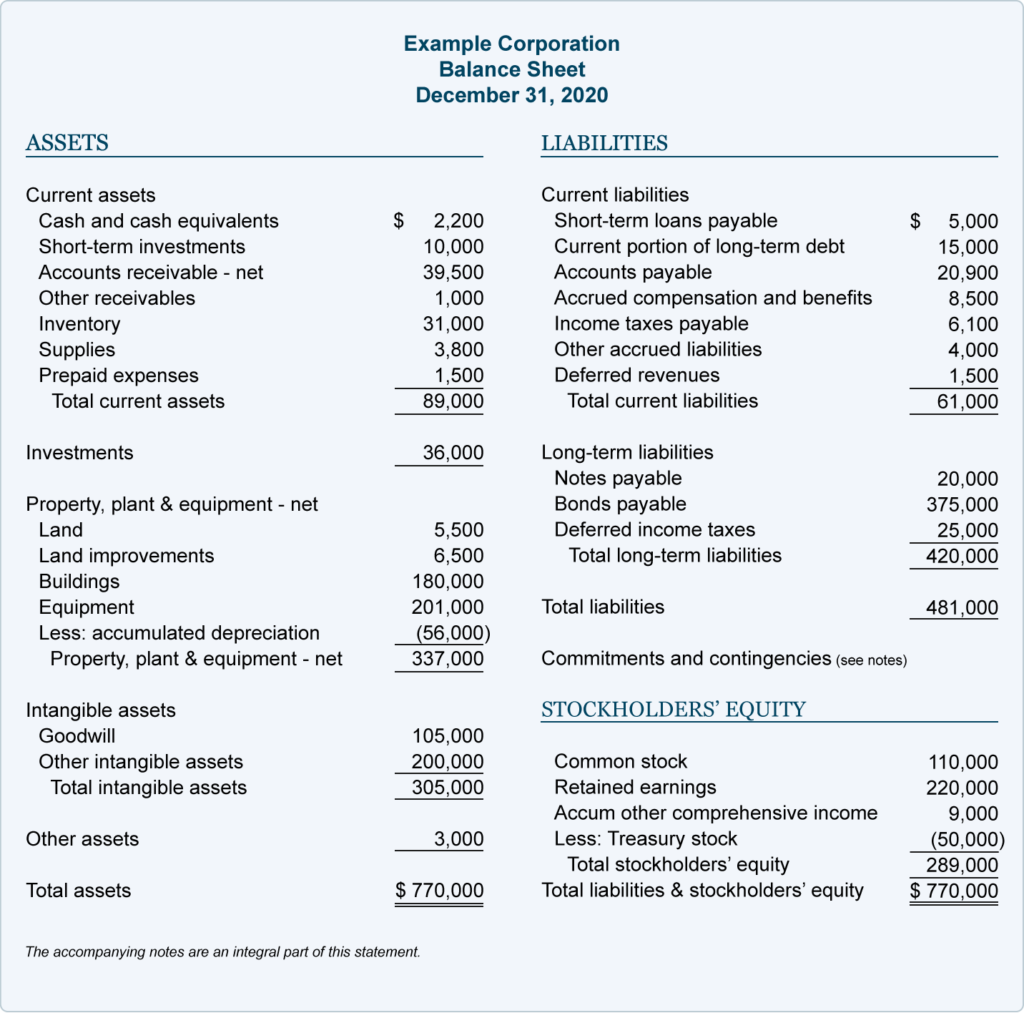

Purpose: The balance sheet provides a snapshot of a company’s assets, liabilities, and shareholders’ equity at a specific point in time. It shows what the company owns and owes.

Key Components:

Assets (Current and Non-current)

Cash and equivalents, Accounts receivable, Inventory

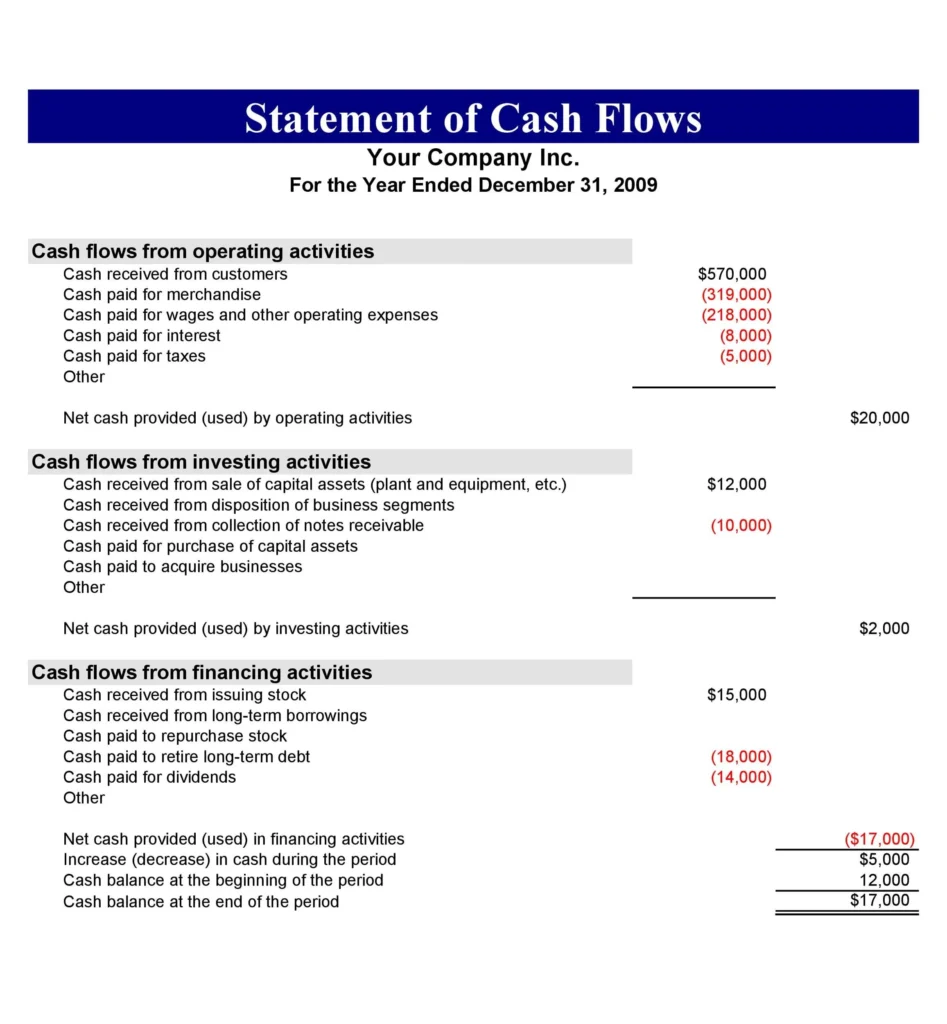

Purpose: The cash flow statement tracks the flow of cash in and out of the business over a period of time. It focuses strictly on actual cash, not accounting entries.

Key Components:

Operating Activities (cash from main business activities)

Investing Activities (cash from buying or selling assets)

Financing Activities (cash from borrowing, repaying debt, or equity transactions)